ITR 7 A.Y.2022-23: In this article, we will discuss ITR-7 instructions, filing procedure, changes, PDF format, FAQ and more. ITR-7 can be used for the persons including companies required to furnish returns under sections 139(4A) or 139 (4B) or 139 (4C) or 139 (4D) only.

Updates: ITR-7 is also now available for efiling. Excel Offline Utility for preparing and filing ITR 7 for AY 2022-23 is released. Please click Downloads | Income Tax Department to access and download the same. Once prepared, you can upload the JSON to the Income-tax website.

Download ITR-7 A.Y. 2022-23

| Utility | Download |

| Download | |

| Excel Utility ITR-7 A.Y. 2022-23 | Download |

Download ITR 7 – PDF, Excel & Java Utility A.Y.2018-19

| Utility | Version | Date | Download |

| Excel | PR4 | 09-08-2018 | Download |

| Java | PR5 | 09-08-2018 | Download |

| Download |

Who can use ITR – 7 Form (A.Y. 2022-23)?

Persons Liable to File ITR-7 (A.Y. 2022-23): ITR-7 Form can be used by persons including companies who are required to furnish income tax returns under section 139(4A) or section 139(4B) or section 139(4C) or section 139(4D) or section 139(4E) or section 139(4F).

Scheme of the Form

The Scheme of this form follows the scheme of the law as outlined above in its basic form. The Form has been divided into three parts. It also has twenty-five Schedules. The details of these parts and the Schedules are as under:-

(i) Part A-GEN mainly seeks general information requiring the furnishing of personal information like name and address, PAN number, date of creation, fling status, other details and audit details ;

(ii) The second part, i.e., Part-B is regarding an outline of the total income and tax computation in respect of income chargeable to tax.

(iii) There are various Schedules details of which are as under-

- Schedule-I: Details of amounts accumulated/ set apart within the meaning of section 11(2) or in terms of third proviso to section 10(23C) in last year‟s viz., previous years relevant to the current assessment year.

- Schedule-J: Statement showing the funds and investments as on the last day of the previous year.

- Schedule-K: Statement of particulars regarding the Author(s)/ Founder(s)/ Trustee(s)/ Manager(s), etc., of the Trust or Institution.

- Schedule-LA: Details in case of a political party. (e) Schedule-ET: Details in case of an Electoral Trust

- Schedule AI: Aggregate of income derived during the previous year

excluding voluntary contributions. This is to be filled by all persons except political party or electoral trust. - Schedule ER: Amount applied to charitable or religious purposes in India or for the stated objects of the trust/institution during the previous year –

Revenue Account. This is to be filled by all persons except political party or electoral trust. - Schedule EC: Amount applied to charitable or religious purposes in India or for the stated objects of the trust/institution during the previous year–

Capital Account [excluding application from borrowed funds and amount exempt u/s 11(1A)]. This is to be filled by all persons except political party

or electoral trust. - Schedule-HP: Computation of income under the head Income from House

Property. - Schedule-CG: Computation of income under the head Capital gains.

- Schedule-OS: Computation of income under the head Income from other sources.

- Schedule-VC: Details of Voluntary Contributions received

- Schedule-OA: General information about business and profession.

- Schedule-BP: Computation of income under the head “profit and gains from business or profession”.

- Schedule-CYLA: Statement of income after set off of current year‟s losses

- Schedule-MAT: Computation of Minimum Alternate Tax payable under section 115JB

- Schedule-MATC: Computation of tax credit under section 115JAA

- Schedule AMT: Computation of Alternate Minimum Tax payable under section 115JC

- Schedule AMTC: Computation of tax credit under section 115JD

- Schedule-PTI: Statement of income from Business Trust or Investment

Fund as per section 115UA, 115UB. - Schedule-SI: Statement of income which is chargeable to tax at special rates

- Schedule 115TD: Accreted income under section 115TD

- Schedule FSI: Details of income accruing or arising outside India

- Schedule TR: Details of Taxes paid outside India

- Schedule FA: Details of Foreign Assets and Income

Guidance for Filling ITR-7

(1) General

- All items must be filled in the manner indicated therein; otherwise the return maybe liable to be held defective or even invalid.

- If any item is inapplicable, write “NA” against that item.

- Write “Nil” to denote nil figures.

- Except as provided in the form, for a negative figure/ figure of loss, write “-” before such figure.

- All figures should be rounded off to the nearest one rupee. However, the figures for total income/ loss and tax payable be finally rounded off to the nearest multiple of ten rupees.

(2) Sequence for filling out parts and Schedules

- Part A

- Schedules

- Part B

- Verification

PART A-GEN

Most of the details to be filled out in Part-Gen of this form are self-explanatory. However, some of the details mentioned below are to be filled out as explained hereunder:-

(a) It is compulsory to quote PAN.

(b) Codes for status:

| Sl. | Status | Code | Sl. | Status | Code |

| i | Individual | 01 | vi | Body of individuals (BOI) | 06 |

|

ii |

Firm (other than the one engaged in profession) |

02 |

vii | Artificial juridical person | 07 |

| iii | Firm engaged in profession | 03 | viii | Co-operative society | 08 |

| iv | Association of persons (AOP) | 04 | ix | Company as per

section 25 of the Companies Act |

09 |

| v | Association of persons (Trust) | 05 | x | Local authority | 10 |

(c) Tax payers are advised to furnish their correct mobile number and e-mail address so as to facilitate the Department in sending updates relating to demand, refund etc. In case a return is filed by an intermediary/professional, the email address of the intermediary as well as the assessee may be provided;

(d) Details of the project/ institution run by you- In this section write the name of the project/institution run by you. For example- If running educational projects/institutions then name of the school/college/university etc. need to be mentioned. Similarly, in case of the hospitals/research institutions the name of the hospital or research centre need to be mentioned. If more than one project/institution is run by the taxpayer, then mention the name of all the projects/institutions. The nature of activity and the classification of the activity engaged by the project/institution should be filed as below. In case the activity/classification falls under more than one head, all such heads may be specified.

| Sl. | Nature of activity | Classification | |

| i | Charitable | a | Relief of the poor |

| b | Education | ||

| c | Medical Relief | ||

|

d |

Preservation of environment (including

watersheds, forests and wildlife) |

||

|

e |

Preservation of monuments or places or objects of artistic or historic

interest |

||

| f | Object of general public utility | ||

| g | Development of khadi or village industries | ||

| ii | Religious | Religious | |

| iii | Research | a | Scientific Research |

| b | Social Research | ||

| c | Statistical research | ||

| d | Any other research | ||

| iv | News Agency | News Agency | |

|

v |

Professional

Bodies |

a |

Law |

| b | Medicine | ||

| c | Accountancy | ||

| d | Engineering | ||

| e | Architecture | ||

| f | Company secretaries | ||

| g | Chemistry | ||

| h | Materials management | ||

| i | Town planning | ||

| j | Any other profession | ||

| vi | Trade union | Trade union | |

| vii | Political | Political party | |

| viii | Electoral trust | Electoral trust | |

|

ix |

Others |

a |

Specified income arising to a

body/authority/Board/Trust/Commission u/s 10(46) |

| b | Infrastructure Debt fund u/s 10(47) | ||

| c | Any other | ||

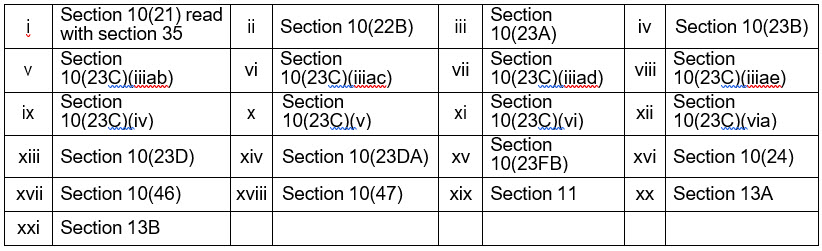

(e) Details of registration or approval- If you are registered under section 12A/12AA, then provide the date of the registration, registration number and the registering authority. If you have received approval under section 35 or section 10(23C), then provide the date of approval, the approval reference number and the approving authority. Section under which exemption claimed in respect of each project/institution to be specified as below:-

(f) Tick in the box to indicate the section under which the return is filed.

(g) All the boxes in the table for “Other Details” need to be filled, if applicable.

- Where one of the charitable purpose is advancement of any other object of general public utility as per section 2 (15) then specify whether such activity is of commercial natu If yes, then specify the aggregate receipts in respect of each institution engaged in such activity, and percentage of receipt from such activity.

- If you have received approval under section 80G then provide the approval reference number and the date of approval.

- If there is any change in the objects or activities during the financial year then tick yes, and fill up details of fresh registration, if any.

- In case of a political party, fill out the details in this column along with Schedule LA.

- In case of Electoral Trust, fill out the details in this column along with Schedule ET.

- If you are registered under Foreign Contribution Regulation Act (FCRA), tick yes and fill up registration number, date of registration, total amount of foreign contribution received during the year. The purpose for which the foreign contribution is received also needs to be specified

(h) In Item no. J, “Audit Information” needs to be filled up. Audit is required to be done under different sections of the Act, including section 10(23C)(iv), 10(23C)(v), 10(23C)(vi), 10(23C)(via), section 12A, section 13A, section 44AB etc. Specify the section under which audit has been done in the space designated for the same in the return and date of furnishing the audit report.

PART B – TI

(a) Item 1 to Item 4ii:- transfer figures from the appropriate Schedule.

(b) Item 4iii to Item 6:- make adjustments as specified and enter the total as narrated in item 7.

(c) Claim of exemption u/s 10 is to be made in items 8, 9 and 10.

(d) The income other than the exempt income u/s 11, 12, 13 and 10 shall form part of the four heads of income and should be entered in Schedule HP, CG, BP & OS and the amount be entered in item 13.

(e) Item 21 to Item 25: total of agricultural income to be mentioned for rate purposes; income chargeable at special rates and maximum marginal rates are to be mentioned separately. Anonymous donations, taxed @ 30%, need to be mentioned separately.