Mutual Fund Taxation A.Y. 2022-23: In case you are planning to invest or have already invested in mutual funds, you need to understand their taxation. You cannot get a better return on mutual funds without knowing the tax rules. You must know how to calculate taxes on mutual fund gains and dividends.

You can find out what taxes are applicable to mutual fund gains in two ways.

- Firstly, there is a manual method in which you should make a note of all the purchasing dates and redemption dates.

- A second one is the automatic generation of capital gains statements by the organizations that manage mutual funds.

In this article, we will discuss how to calculate short-term and long-term capital gains and dividends from mutual funds manually. Let’s start to understand the concept tax on mutual funds step by step.

Table of contents

Taxes on Mutual Fund Capital Gains

Types of Capital Gains

Firstly, you should be aware of the fact that taxes are imposed on both income and gains. In the case of mutual funds, our gains or income will be in the form of dividends or capital gains. Firstly, let’s take a look at the tax implications of capital gains on mutual funds. We normally buy mutual funds in order to be able to sell them at a higher price at some point in the future. This is what is referred to as capital gains when it comes to mutual funds. Capital gains are profits from selling or redeeming a mutual fund at a higher value than the price at which it was purchased.

For example: Buying mutual funds units at Rs.245 and selling them at Rs. 255/- will result in a capital gain of Rs.10.

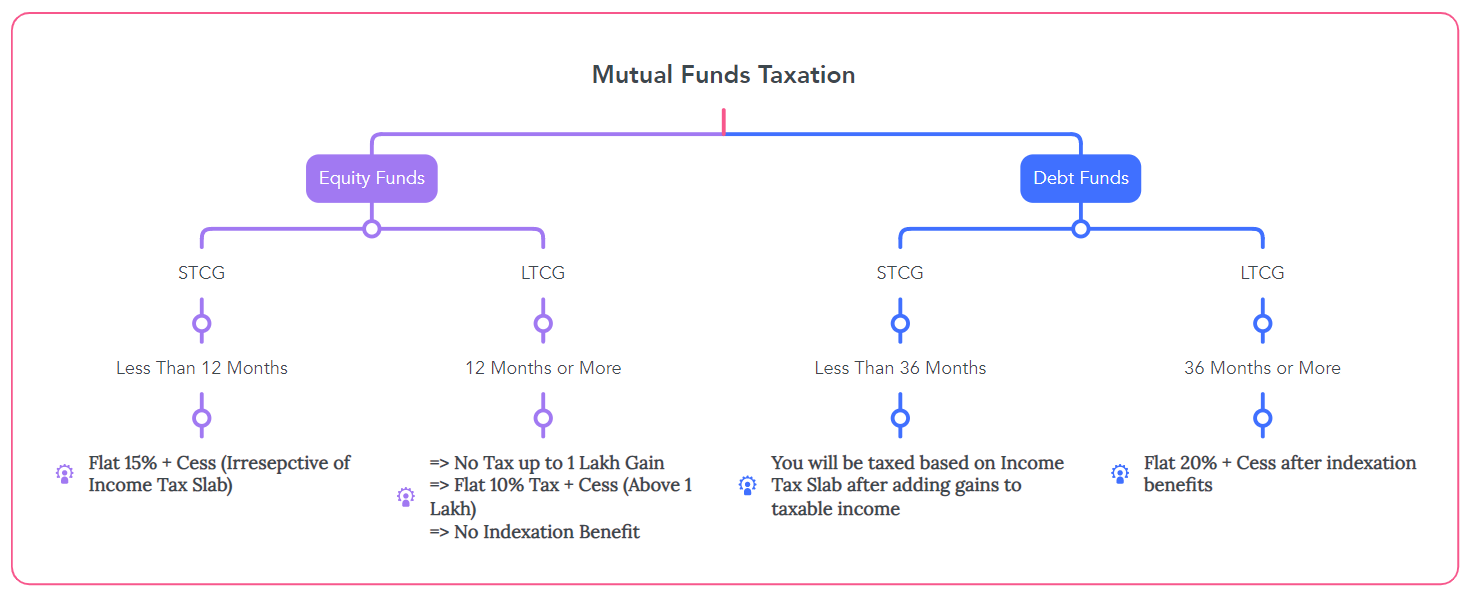

- In the case of mutual funds, there are two types of gains you can make when you redeem your mutual funds, namely short-term capital gains and long-term capital gains.

- Your mutual fund holding period determines whether you have made short-term or long-term capital gains.

- It is the time period between the time of purchase and the time of redemption.

Types of Mutual Funds

In order to better understand mutual fund taxation, it is important that we understand the types of mutual funds and their taxation rules. To begin, let us examine the three factors that influence the tax liability of mutual funds. To calculate taxes on mutual funds, we divide the mutual funds into two categories i.e. equity and debt mutual fund. It is important to note that the tax treatment of equity funds and debt funds, especially in terms of holding periods, is totally different.

To determine whether it is a short-term capital gain or long-term capital gain, please refer to the table below.

| Mutual Fund Types | Short-term Capital Gains Period | Long-term Capital Gains Period |

| Equity Funds | Less than 12 months | 12 months or over |

| Debt Funds | Less than 36 months | 36 months or over |

| Hybrid Equity Fund | Less than 12 month | 12 months or over |

| Hybrid Debt Fund | Less than 36 months | 36 months or over |

Note: We will calculate the capital gain on mutual funds only when we sell these units or redeem these units. You can say that you won’t pay any taxes until you redeem your mutual funds.

Capital Gains Tax Rates on Mutual Fund

After reading the discussion above, you should now have a better understanding of the concept of short-term capital gains as well as long-term capital gains when investing in mutual funds. The next step is to discuss the taxes that are applicable to these gains. The following table shows how mutual funds’ long-term and short-term capital gains are taxed.

Table for Calculating Short-Term or Long-Term Capital Gains:

| Mutual Fund Type | Tax on Short-Term Capital Gains | Tax on Long-Term Capital Gains |

| Equity Funds | 15% + Cess | Up to Rs. 1 Lakh Exemption (After 1 Lakh 10%) + Cess |

| Debt Fund | As per Income Tax Slab | 20% + Cess (Indexation Benefit Available) |

| Hybrid Equity Fund | 15% + Cess | Up to Rs. 1 Lakh Exemption (After 1 Lakh 10%) + Cess |

| Hybrid Debt Fund | As per Income Tax Slab | 20% + Cess (Indexation Benefit Available) |

Taxation on Equity Schemes Funds

Equity Schemes – Short-Term Capital Gains: According to the above table, the short-term capital gain (STCG) on equity funds is flat at 15% plus the education cess. The following example will help you better understand short-term capital gains taxation on equity mutual funds.

- STCG 15% + Cess (Section 111A)

- Example: STCG Rs.130000 – The tax will be calculated on Rs. 130000 @ 15% i.e. 19500 (plus cess and surcharge as applicable).

In the case of short-term capital gains, you are not eligible for a 1 lakh exemption.

Equity Schemes – Long-Term Capital Gains: According to the above table, the long-term capital gain (LTCG) on equity funds is flat at 10% in excess of Rs. 1 Lakh. In the case of short-term capital gains, the exemption of Rs.1 lakh is not available. The following example will help you better understand long-term capital gains taxation on equity mutual funds.

- LTCG 10% in excess of Rs.1 Lakh (Section 112A)

- Example: LTCG Rs.130000 – The tax will be calculated on Rs.30,000 @10% i.e. Rs.3000 (plus cess and surcharge as applicable).

There is no benefit of indexation.

Taxation on Debt Schemes Funds

Debt Schemes – Short-Term Capital Gains: According to the above table, the short-term capital gain (STCG) on debt funds will be taxed as per the income tax slab of the assessee. The following example will help you better understand short-term capital gains taxation on debt mutual funds.

- STCG – As per Income Tax Slab.

- For Example: Suppose you already make over Rs.5,00,000 excluding STCG and you’re in the 20% tax bracket, your short-term capital gains tax rate will be 20% (plus cess and surcharge).

Debt Schemes – Long-Term Capital Gains: LTCG tax on debt-oriented schemes is charged at 20% under section 112 of the Income Tax Act, 1961. Tax departments provide the Cost Inflation Index (CII) to adjust the purchase cost for price rises (inflation).

- LTCG – 20% with indexation benefits (Section 112)

- Indexed Cost of Acquisition = [CII for the year of sale ÷ CII for the year of purchase (or CII for 2001–02, whichever is earliest)] x cost of acquisition – Check Here Cost Inflation Index Table

Taxation on Equity Linked Saving Schemes (ELSS)

As per section 80C of the income tax act, equity-linked saving schemes are eligible for tax deductions up to Rs.1,50,000. There is a 3-year lock-in period for equity-linked savings schemes. It is not possible for you to withdraw any money from these mutual funds until 3 years after the date you purchased them.

- Capital gains are automatically treated as long-term after a lock-in period of three years.

Taxation on Hybrid Mutual Fund

There are two types of hybrid funds i.e. equity-oriented or debt-oriented. Generally, equity-focused hybrid funds have more than 65% equity exposure, while all other hybrid funds are debt-focused funds. Hybrid equity-focused and debt-focused schemes follow the same tax rules as equity schemes and debt schemes.

Equity Focused Hybrid Fund:

- STCG 15% (Section 111A) Example: STCG Rs.130000 – The tax will be calculated on Rs. 130000 @ 15% i.e. 19500 (plus cess and surcharge as applicable). In the case of short-term capital gains, you are not eligible for a 1 lakh exemption.

- LTCG 10% in excess of Rs.1 Lakh (Section 112A) Example: LTCG Rs.130000 – The tax will be calculated on Rs.30,000 @10% i.e. Rs.3000 (plus cess and surcharge as applicable). There is no benefit of indexation.

Debt-Focused Hybrid Fund:

- STCG – As per Income Tax Slab. Suppose you already make over Rs.5,00,000 excluding STCG and you’re in the 20% tax bracket, your short-term capital gains tax rate will be 20% (plus cess and surcharge).

- LTCG – 20% with indexation benefits (Section 112) Indexed Cost of Acquisition = [CII for the year of sale ÷ CII for the year of purchase (or CII for 2001–02, whichever is earliest)] x cost of acquisition

Tax on Dividends of Mutual Funds

This is another tax regulation which is applicable to the receiving of dividends from mutual funds. When you receive dividends from a mutual fund you invest in, you must pay tax. In terms of taxation, the old and new rules on dividends from mutual funds are totally different. Let’s discuss the tax on dividends of mutual funds.

- Dividend Distribution Tax was withdrawn by the Finance Act, 2020. Before March 31, 2020, mutual fund dividends were tax-free.

- It has recently been decided that the entire dividend income of an investment will now be taxable in the hands of the investor under the heading of “Income from other sources.” So, the dividend on mutual funds will be taxable as per your income tax slab.

TDS on Dividends of Mutual Funds: Dividends paid in excess of Rs.5000 during any financial year are now subject to 10% TDS deduction under section 194K. When filing his income tax return, the investor can claim this TDS.

Automatically Download Capital Gains Statement of Mutual Funds

We know it is a little bit difficult task for the assessee to make a capital gains statement manually after reading all the above rules and instructions. But it is very easy now to download capital gains statements automatically from the CAMS, Kfintech and mutual funds organisation official websites. Suppose you have invested in SBI mutual funds then you can download the capital gains statement by visiting the official website of SBI mutual funds.

You can download all mutual fund capital gains statements that are registered on your PAN by visiting CAMS online or fintech. Please follow the below links to download mutual fund short-term and long-term capital gains statements including SIP.

- https://www.camsonline.com/Investors/Statements/Capital-Gain&Capital-Loss-statement – Visit Here

- https://mfs.kfintech.com/investor/General/CapitalgainsbyEmailid – Visit Here

You can also check TDS on dividends by downloading form 26AS. Please follow the below links to know how to download the 26AS statement to check the TDS on dividends of all mutual funds.

- https://alerttax.in/view-form-26as/ – Visit Here

Taxation on Mutual Fund SIP

The taxation rules on Mutual Funds Systematic Investment Plan (SIP) are the same as on lumpsum mutual funds. The same rules will be applicable to equity and debt fund. If you are planning to invest in SIP, it is crucial that you understand the tax implications on the purchase and sale side of the transaction in order to make the right decisions.

There may be short-term capital gains and long-term capital gains in one SIP. As per the date of purchase and sale, every investment is treated as a new investment in SIP. More than 12 months of Investment in Equity Finds will be treated as long-term capital gains.

For Example: Suppose you start SIP of Rs. 5000/per month (Starts from 21-04-2021) – Sale of All Units on 22-04-2022

| Date Purchase | Units | Rate | Value | Sell Rate | LTCG | STCG |

| 21-04-2021 | 100 | 50 | 5000 | 110 | 6000 | |

| 21-05-2021 | 100 | 50 | 5000 | 110 | 6000 | |

| 21-06-2021 | 90.90 | 55 | 5000 | 110 | 5000 | |

| 21-07-2021 | 86.20 | 58 | 5000 | 110 | 4482 | |

| 21-08-2021 | 83.33 | 60 | 5000 | 110 | 4167 | |

| 21-09-2021 | 76.92 | 65 | 5000 | 110 | 3461 | |

| 21-10-2021 | 71.42 | 70 | 5000 | 110 | 2857 | |

| 21-11-2021 | 66.66 | 75 | 5000 | 110 | 2333 | |

| 21-12-2021 | 62.50 | 80 | 5000 | 110 | 1875 | |

| 21-01-2022 | 55.55 | 90 | 5000 | 110 | 1111 | |

| 21-02-2022 | 50 | 100 | 5000 | 110 | 500 | |

| 21-03-2022 | 47.61 | 105 | 5000 | 110 | 238 | |

| Totals | 6000 | 32024 |

The purpose of this article is to explain to you the concept of taxation on mutual funds. You are welcome to contact us via the comment form if you have any questions related to short-term capital gains tax or long-term capital gains tax on mutual funds.

When dividend is received and after that if a fund is sold how dividend income impact the capital gain. Is there any rule pertaining to selling of fund post receiving the dividend.